Interest rates cut to 3.75% but further reductions to be ‘closer call’

Here is the enhanced and rewritten article, tailored for Brainx Ultimate with a professional, journalistic tone, expanded analysis, and strict adherence to your formatting requirements.

Bank of England Slashes Rates to 3.75%: A Pivotal Shift in the UK’s Economic Battle

Brainx Perspective

At Brainx, we believe this latest rate cut is a double-edged sword that exposes the fragile state of the British economy. While it offers immediate, tangible relief to borrowers and mortgage holders, the sheer necessity of this cut—driven by stalling growth rather than booming prosperity—signals that the road to full economic recovery remains steep and uncertain for policymakers.

The News: A Deep Dive into the Decision

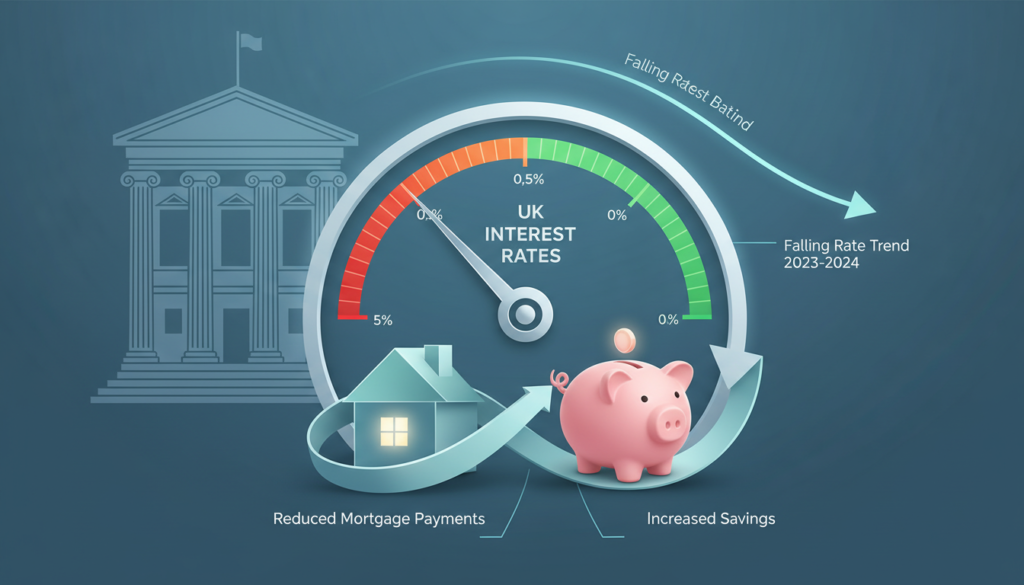

The Bank of England has officially lowered its benchmark interest rate to 3.75%, a move that places borrowing costs at their lowest point in nearly three years. This critical decision comes as the Monetary Policy Committee (MPC) attempts to navigate a complex economic landscape characterized by sluggish expansion, rising unemployment fears, and a cooling inflation rate.

While the reduction provides breathing room for millions of households, the decision was far from unanimous. It reflects a central bank that is cautiously optimistic yet acutely aware of the risks that lie ahead in 2026.

Key Developments

- The Verdict: The benchmark rate has been cut from 4% to 3.75%.

- The Vote: The decision was razor-thin, approved by a 5-4 margin within the MPC. This split vote highlights significant internal disagreement regarding the speed at which rates should fall.

- Inflation Outlook: Inflation is now projected to hit the 2% target by next year, earlier than previously anticipated.

- Economic Stagnation: The cut is a response to fears of “zero growth” in the final quarter of the year.

- Future Outlook: Governor Andrew Bailey signaled a “gradual downward path” but refused to commit to a specific timeline for further cuts.

The Mechanics of the Split Vote

The 5-4 vote is particularly telling. A margin this narrow suggests that nearly half of the committee remains terrified of inflation reigniting. While the majority voted to stimulate the economy to prevent a recession, the dissenters likely argued that wage growth remains too strong to justify loosening the reins just yet. This tension suggests that while the direction of travel is down, the pace will be agonizingly slow and data-dependent.

Economic Analysis: The Growth vs. Inflation Trade-off

The primary driver behind this decision is the rapid cooling of the UK economy. The Bank’s assessment described recent performance as “lacklustre,” a polite term for an economy that has effectively stalled.

The Inflation Picture

The “good news,” as acknowledged by Governor Andrew Bailey, is that price rises are slowing down.

- Current Rate: Annual inflation slowed to 3.2% in November.

- The Target: The Bank aims for 2%, a figure they now believe is achievable sooner than expected.

However, the path to 2% is not linear. Energy prices, global supply chain disruptions, and domestic wage settlements all pose risks that could force the Bank to hit the brakes on future cuts.

The Growth Problem

Why cut rates now if inflation is still above 3%? The answer lies in the “zero growth” forecast. High interest rates work by suppressing demand—making it expensive to borrow and invest. The Bank has realized that demand has been suppressed so effectively that the economy is barely moving.

- Business Sentiment: Companies are expressing anxiety over market conditions, leading to reduced investment.

- Consumer Behavior: Shoppers are “keenly focused on value for money,” resulting in smaller basket sizes at supermarkets.

- Hospitality Sector: Even the Christmas period, usually a boom time for pubs and restaurants, has seen businesses scrambling to cut costs as customers tighten their belts.

Impact on Your Wallet: Winners and Losers

A change in the base rate triggers a domino effect across the financial ecosystem, creating distinct winners and losers among the public.

1. Mortgage Holders: A Mixed Bag

The most immediate impact will be felt in the housing market, though not everyone will benefit equally or at the same time.

- Tracker Mortgages: Approximately 500,000 homeowners on tracker mortgages will see an almost immediate benefit. A typical monthly repayment could drop by around £29.

- Standard Variable Rates (SVR): Borrowers on SVRs should also see reductions, though it is up to individual lenders to pass these on fully.

- Fixed-Rate Deals: The majority of UK homeowners are on fixed-rate deals. They will see no immediate change. However, those looking to remortgage in the coming year may find the landscape much more favorable than it was six months ago.

Case Study: Consider Kayleigh Taylor, a homeowner who remortgaged during the peak of the rate hike cycle. Her payments skyrocketed, putting immense strain on her family finances. With this cut, and the promise of more to come, she is now reconsidering her future. Instead of downsizing, her family is cautiously exploring moving to a larger property, hoping that by the time their current deal expires next year, rates will have normalized further.

2. Savers: The Downside

For every borrower celebrating, a saver is losing out. Banks are typically quick to slash interest rates on savings accounts following a Bank of England cut.

- Retirees: Those relying on interest income from cash savings will see their monthly returns diminish.

- Strategy Shift: This environment often forces savers to look toward the stock market or bonds to find yields that beat inflation, introducing more risk to their portfolios.

The Political Arena: A War of Words

Interest rates are technically independent of politics, but their consequences are deeply political. The reaction from Westminster highlights how both major parties are using the economy as a battleground.

- The Government’s Stance: The Chancellor has seized upon this as a victory, noting it is the sixth rate cut since the election. Framing this as the “fastest pace of cuts in 17 years,” the government is keen to present this as evidence that their economic plan is working and that the “cost of living crisis” is abating.

- The Opposition’s Counter: The Shadow Chancellor offers a contrasting narrative. While welcoming the relief for families, they argue that the necessity of such cuts underscores the “fragility” of the economy. In their view, the cuts are a symptom of “economic mismanagement” that has stifled growth, rather than a sign of triumph.

Why It Matters

This rate cut signals the end of the “fighting inflation at all costs” era and the beginning of a new phase focused on reviving a stalled economy. For the common man, it means the worst of the borrowing crunch is likely over, but it also serves as a warning that the economy remains weak, with job security and wage growth likely to become the next major concerns.

Leave a Reply